In case you’ve obtained a house fairness line of credit score (HELOC), cost aid might lastly be right here.

The Fed is anticipated to “pivot” as we speak, which means they’ll shift from a tightening financial coverage to a loosening coverage.

In different phrases, they’re going to begin reducing charges as a substitute of elevating them!

Whereas this received’t have a direct affect on long-term mortgage charges, it straight impacts loans tied to the prime price, together with HELOCs.

This implies your HELOC price will go down by regardless of the Fed cuts. So in the event that they reduce 25 foundation factors as we speak, your HELOC price might be adjusted down 0.25%.

Although one reduce isn’t probably to supply main aid, there are expectations that that is the primary reduce of many, with probably 200+ bps of cuts penciled in over the following 12 months.

So if you happen to’ve been given the choice to “lock your HELOC price,” it’s in all probability finest to provide it a tough cross.

How HELOC Charges Are Decided

As a fast refresher, HELOCs are variable-rate loans, which means they’ll alter every month based mostly on the prime price.

To come back together with your HELOC price, you mix the HELOC’s margin, which is mounted, and the prevailing prime price, which strikes in lockstep with the fed funds price.

Every time the Fed decides to boost or decrease its personal fed funds price (FFF), the prime price can even go up or down by the identical quantity.

Since early 2022, the Fed has raised the FFF 11 instances, from near-zero to a spread of 5.25% to five.50%.

Right this moment, they’re anticipated to decrease the FFF both 25 or 50 bps. This implies banks will decrease the prime price by the identical quantity shortly after.

Fast notice: The Fed doesn’t management long-term mortgage charges, so their motion as we speak received’t straight affect the 30-year mounted. In the event that they reduce the 30-year mounted may truly rise as we speak!

Anyway, let’s assume you’ve got a margin of two% and prime is at present 8.50%. That’s a ten.50% HELOC price. Ouch!

But when the Fed cuts 25 bps or 50 bps as we speak, that price will fall to 10.25% or 10%. Okay, we’re getting someplace.

Nonetheless not a low price, although it’s lastly not going up and in reality is coming down.

Now consider one other 200 bps of cuts and the speed is down to eight%. Candy, that might truly lead to some respectable curiosity financial savings and a decrease month-to-month cost!

What Is Locking Your HELOC Anyway?

That brings us to “locking your HELOC.” As famous, HELOCs are variable-rate loans.

However the banks will generally provide the alternative to lock the rate of interest in for the rest of the mortgage time period. This occurred to my pal, who requested as we speak if he ought to lock in his price.

This solely occurs when you’ve had the HELOC open for a time period and made attracts on it. Not upfront, in any other case that’d merely be a fixed-rate dwelling fairness mortgage.

So Financial institution X may say hey, we all know charges have been rising and there’s quite a lot of uncertainty on the market.

In case you don’t wish to take care of any additional changes, you may lock within the price you at present have.

For these not listening to the Fed, this may sound like a good concept. In any case, many owners are risk-averse, which is why in addition they don’t are likely to go together with adjustable-rate mortgages.

And plenty of debtors might not have truly recognized that their HELOC was variable to start with.

They might leap on the provide to lock within the price and cease worrying. However this might truly be a horrible time to do this.

You watched helplessly as your HELOC went up and up over the previous couple years. And now you’re going to lock it in, when charges are lastly slated to fall?

In all probability not a good suggestion. This may simply profit the financial institution, who will make lots much less if you happen to merely do nothing and let the speed fall as prime drifts decrease and decrease over the following 12 months.

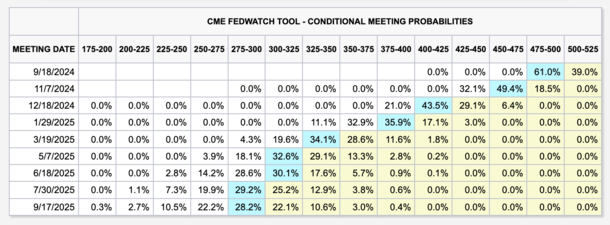

In case you’re curious the place the prime price is anticipated to go, control the fed funds price predictions. A superb place to do this is the CME web site.

They’re at present predicting a first-rate price that’s 2.25% decrease by September seventeenth, 2025, as seen within the desk above.

In different phrases, when you’ve got a HELOC set at 10% as we speak, it could be 7.75% in 12 months. Don’t lock within the 10% price and miss out on these financial savings!

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and current) dwelling patrons higher navigate the house mortgage course of. Comply with me on Twitter for decent takes.