Just lately, I’ve been getting numerous questions on inflation. Is it coming? How unhealthy will or not it’s? And, in fact, what ought to I do about it? It has been fascinating, as a result of inflation has been largely off the radar for some years—it merely has not been an issue. What has been driving the priority now appears to be worries in regards to the results of the federal stimulus applications, which many assume will drive extra inflation. However I don’t assume so. To indicate why, let’s return to historical past.

Client Value Index

All objects. Let’s begin with the complete Client Value Index, together with all objects. Over the previous 20 years, inflation has averaged round 2.5 %, on a year-on-year foundation. Earlier than the nice monetary disaster, inflation ranged round 2 % to three %; there was a spike to over 5 %, popping out of the disaster. Since then, for the previous decade, the common has been round 1 % to 1.5 %, and the very best degree has been round 2.5 %. Observe the very best degree of the previous decade was the common of the earlier decade. Inflation has been trending down.

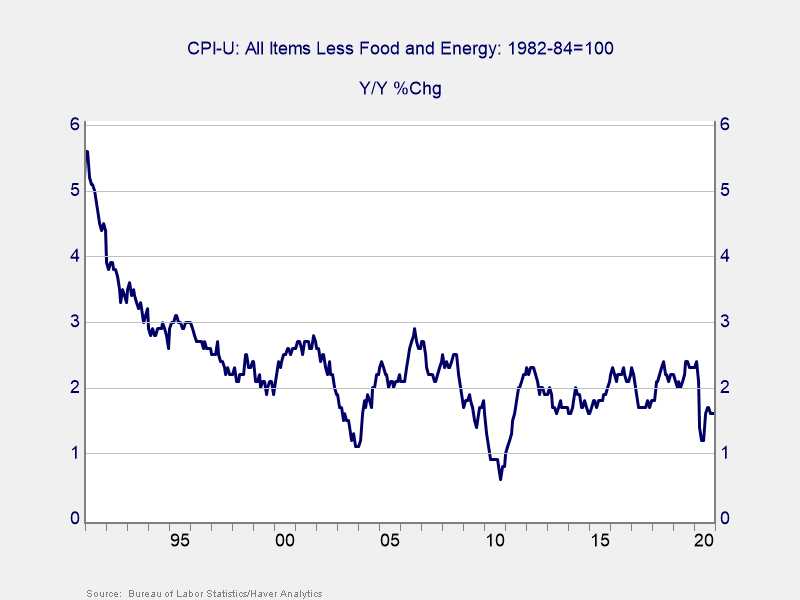

Much less meals and vitality. A greater indicator of basic value inflation, nevertheless, is core inflation, which takes out two extremely variable objects: meals and vitality. Right here, we are able to see inflation is decrease and extra constant: round 2 % for the previous twenty years, and ranging between 2 % and three %. Proper now, we’re at about 1.5 %, not too far off from the common.

This historical past is the context for what we are going to seemingly see over the subsequent yr or so. The 20-year interval above contains a number of episodes of contraction and restoration, together with a number of episodes of financial stimulus and financial stimulus. But inflation remained remarkably steady. Once we look forward, we now have to contemplate what’s prone to occur and examine it with what has already occurred.

The Federal Deficit

To my thoughts, probably the most fast comparability to the present stimulus bundle is the federal deficit over the previous 20 years. Deficit spending, typically, is the federal government spending cash it doesn’t have. To the extent this pushes up demand, with out pushing up accessible provide, it ought to create inflation. The stimulus, in any case, is simply extra deficit spending. So, if deficit spending and inflation are positively correlated, then the stimulus will seemingly push inflation up.

That situation shouldn’t be what we see, nevertheless. The correlation is constructive, as proven within the chart above. However due to the way in which the chart is constructed, meaning because the deficit will get greater, the inflation price really drops. In different phrases, a bigger deficit, over the previous 20 years, has meant a decrease inflation price. Because the stimulus bundle will increase the deficit, per this relationship, it ought to drive inflation decrease—not greater.

I don’t really consider that, thoughts you, as correlation is famously not causation. What I do take away from it’s that historical past doesn’t inform us that the stimulus will essentially trigger inflation. Inflation shouldn’t be inevitable right here. So, what does it inform us?

Inflation Relies on Demand

Historical past tells us that inflation relies upon extra on demand and that when demand collapses in a disaster, so does inflation, even with the upper deficit spending. Submit-2000, we noticed the deficit enhance and inflation drop, solely to see the pattern reverse because the financial system recovered. In 2008–2009, we noticed the identical factor, because the deficit spiked and inflation dropped, solely to get better when the financial system normalized. This time, we now have seen the primary half, with the deficit rising and the Client Value Index dropping, and we are going to see the second half shortly because the financial system recovers. Inflation will go up once more.

Take a look at the Developments

However the last factor historical past exhibits us is that as inflation recovers, it doesn’t run previous earlier typical ranges for very lengthy. Submit-2000, inflation rose briefly to comparatively excessive ranges, then subsided once more. Submit-2008, the identical factor. We are able to count on the identical in 2021 and 2022, beginning within the subsequent couple of months. As year-on-year inflation comparisons look again to the preliminary financial drop of the pandemic, they may spike. However because the year-ago comparisons get extra wholesome, the adjustments will drop again once more—simply as we noticed within the final two crises.

At that time, because the financial system normalizes and as individuals and companies return to regular conduct (“regular” outlined as kind of what we now have completed for the previous decade), inflation will then pattern again to that very same regular degree, on this case about 2 %. Sure, that is above the place we at the moment are, however the place we at the moment are nonetheless displays the pandemic. A restoration to regular could be simply that, regular.

So, Will Inflation Go Up?

Sure, it is going to. Will it threaten the financial system or markets? No, as a result of greater inflation will merely replicate a transfer again to the conventional of the previous decade. And that’s one thing we should always all be hoping for.

Editor’s Observe: The authentic model of this text appeared on the Unbiased Market Observer.