I exploit the free Constancy retirement planning software to regulate our present investments relative to our spending. Utilizing that software revealed two basic drivers of monetary success in retirement.

| Good Returns | Unhealthy Returns | |

|---|---|---|

| Low Spending | OK | OK |

| Excessive Spending | OK | Not OK |

Though my spouse mentioned the 2 basic drivers have been solely too apparent, the planning software offers us an thought of how low is low and the way excessive is excessive.

Typical Retirement Calculator

The Constancy retirement planning software makes use of a traditional method. It gathers your investments and asks you ways a lot you propose to spend. Then it simulates future returns to see how nicely your investments will cowl your deliberate spending. It’s successful in case your projected stability is above zero on the finish of your planning horizon. Many retirement planning instruments work like this. I simply occur to make use of the one from Constancy as a result of it’s obtainable and free.

It isn’t straightforward to make use of the software to mannequin large monetary selections equivalent to staying in a high-cost-of-living space after retirement versus relocating as we did final time in Transferring to Decrease Price of Residing After You Retire. You possibly can run the projections and save the report as a PDF, change the assumptions, run it once more, save the brand new report as a PDF, and evaluate the 2 PDFs. In case you’d like to return to your authentic assumptions, it’s essential to keep in mind the place you made modifications and again out all of your modifications.

Once I evaluate the results of various ranges of spending, I exploit my login to run one stage of spending and my spouse makes use of her login to run a distinct stage of spending. Then we evaluate the 2 PDFs. It really works for a easy A-B comparability but it surely’s troublesome to do greater than that.

MaxiFi

Different monetary planning functions are higher geared up for tactical planning. MaxiFi is one in all them.

MaxiFi is on-line monetary planning software program from an organization led by Boston College economics professor Larry Kotlikoff. The Normal model prices $109 for the primary yr ($89/yr for renewal) and the Premium model prices $149 for the primary yr ($109/yr for renewal). I purchased the Premium model final yr to see the way it labored.

I performed with the software program however I’m not an influence person. Reader Dennis Hurley is extra skilled with MaxiFi. He helped me rise up to hurry. I’m solely describing how I used MaxiFi. It will not be the formally appropriate approach as supposed by the software program maker. I’m not paid by MaxiFi or anybody else to put in writing this evaluation. I don’t profit financially in any approach should you purchase MaxiFi or some other software program.

MaxiFi takes an unconventional method. It doesn’t hyperlink your accounts. It solely asks for the full quantity in your pre-tax, Roth, and taxable buckets. It doesn’t ask what investments you’ve gotten in your accounts. You enter your anticipated protected return for every bucket within the settings. It doesn’t ask how a lot you propose to spend except it’s one-time or episodic (“particular bills”). The software program calculates your obtainable discretionary spending primarily based on the precept of consumption smoothing.

Discretionary spending in MaxiFi is in financial phrases. It isn’t what we usually consider as discretionary in on a regular basis life. MaxiFi treats housing, taxes, Medicare Half B premiums, life insurance coverage, and particular bills as fastened spending. All the things else is discretionary spending. You’ll assume meals isn’t discretionary however that’s simply how MaxiFi categorizes issues. If the time period “discretionary” bothers you, simply give it a distinct title or just name it “different.” Discretionary spending in MaxiFi represents a residing normal.

Base Plan and Maximized Plan

MaxiFi begins by asking about your present monetary state of affairs and your assumptions for inflation, anticipated returns, your required retirement age, when you’ll begin withdrawing out of your retirement accounts, and if you’re considering of claiming Social Safety. This generates a Base Plan.

Then it gives to enhance the Base Plan by routinely testing modifications to when you’ll declare Social Safety, when you’ll begin clean withdrawals out of your retirement accounts, whether or not you’ll withdraw from pre-tax accounts first or Roth accounts first, and whether or not you’ll think about shopping for an annuity.

You possibly can say sure or no to which merchandise you need the software program to alter. MaxiFi will generate a Maximized Plan by testing completely different combos of these gadgets and selecting a plan that has the best lifetime discretionary spending. In case you’re proud of the modifications, you possibly can apply them to the Base Plan in a single click on.

Discretionary Spending as a Metric

MaxiFi sees a change as an enchancment when it will increase the calculated discretionary spending. I deal with the annual discretionary spending from MaxiFi solely as a metric. I see it as a residing normal obtainable to me, not because the software program mandating that I have to really spend that quantity yearly. I solely use the quantity of discretionary spending to match completely different conditions. I do know {that a} transfer is an efficient one if it will increase my obtainable discretionary spending.

Social Safety Claiming Technique

In case you’re married and also you set the utmost age to 98 or 100 for each of you, MaxiFi will most probably recommend that you simply each delay claiming Social Safety to age 70. Don’t be shocked if you see it differs from the output of different instruments equivalent to Open Social Safety.

Open Social Safety makes use of mortality tables with weighted chances of residing to completely different ages. MaxiFi makes use of fastened ages out of your inputs. In case you say each of you’ll dwell to 100 for positive, the most effective technique naturally is to delay to age 70 for each. You’ll see completely different methods if you create completely different profiles with each spouses residing to 85 or one partner residing to 95 and the opposite residing to 83, and so forth. I like Open Social Safety’s method higher on this regard.

The utmost age inputs additionally have an effect on annuity strategies within the Maximized Plan. In case you say each of you’ll dwell to 100 within the profile, shopping for an annuity will naturally be useful should you activate optimizing annuities. I set the annuity choices to “no” after I run a Maximized Plan.

Assumptions, Assumptions, Assumptions

MaxiFi is a modeling software. It could possibly’t predict the long run. No software program can. All outputs are primarily based on a selected set of assumptions. I routinely add “primarily based on this set of assumptions” to each output I learn from MaxiFi.

The Maximized Plan is perfect solely primarily based on one set of assumptions. The optimum plan might be completely different beneath a distinct set of assumptions. I see the worth of MaxiFi not as a lot in producing a withdrawal and spending plan primarily based on a set of assumptions however extra in testing completely different assumptions.

Different Profiles

MaxiFi makes it straightforward to match completely different situations. You duplicate the Base Profile into an Different Profile, make modifications within the Different Profile, and evaluate it with the Base Profile. You possibly can have as much as 25 different profiles and evaluate between completely different profiles. This helps reply all types of “Can I afford it?” and “Ought to I do A or B?” questions:

Can I retire now versus 5 years from now?

Can I afford to purchase an costly home or a second residence?

Will serving to my children derail my retirement?

Ought to I promote investments and understand capital good points to pay money for a house or get a mortgage?

Ought to I keep in my present residence or downsize or relocate?

Ought to I promote my home or hire it out as a result of my mortgage is under 3%?

These large monetary selections require extra consideration as a result of they are typically one-time, all-or-nothing, and expensive to modify.

You’ll see the affect in your obtainable discretionary spending if you evaluate outputs between different profiles. You already know you’ll have extra money to spend should you work one other 5 years, however by how a lot? You create one profile with retiring now, duplicate it, change the retirement date, and evaluate. You already know you’ll have much less cash for retirement should you assist your children or grandkids, however by how a lot? You duplicate your present profile into another profile, add the additional bills, and evaluate it together with your present profile.

Instance

A reader mentioned he was inquisitive about transferring from a excessive cost-of-living space however promoting his residence will set off taxes on a big capital acquire nicely past the $500k tax exemption. The NYT buy-or-rent calculator I utilized in the earlier put up doesn’t have in mind the built-in capital acquire. MaxiFi does.

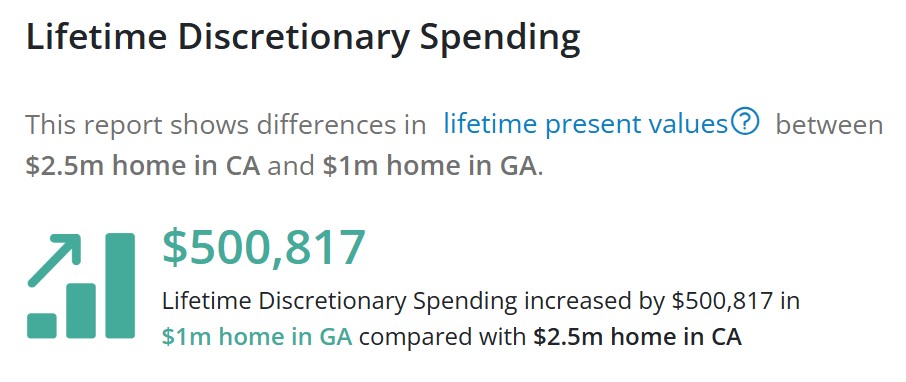

I created one hypothetical profile in MaxiFi with a house in California value $2.5 million having a price foundation of $500k ($2 million unrealized capital acquire earlier than the tax exemption). I duplicated it into one other profile and made modifications to promote the house in California, pay federal and state taxes on the capital good points, and purchase a $1 million residence in Georgia. MaxiFi reveals this after I in contrast the 2 profiles:

It reveals how a lot the lifetime discretionary spending would enhance primarily based on a set of assumptions by promoting the California residence and transferring to Georgia regardless of having to pay capital good points taxes on $2 million. I can create further profiles and evaluate once more with the house worth rising quicker in California than in Georgia or completely different inflation charges and completely different funding returns.

MaxiFi can’t predict the long run however it might probably provide help to mannequin completely different situations.

Roth Conversions

You can even use different profiles to mannequin Roth conversions. MaxiFi doesn’t recommend how a lot it is best to convert however you possibly can take a look at changing completely different quantities between age X and age Y in different profiles. Right here’s a video from MaxiFi on find out how to mannequin a Roth conversion:

Ignore the Precision

Any modeling software program will calculate to the precise greenback however I ignore the precision. As a result of projections are primarily based on assumptions, will probably be a miracle if a projection will get the primary two digits appropriate in actual life. It’s troublesome to even get the primary one digit proper.

Within the earlier instance, if a retired couple sells a $2.5 million residence in California and strikes to Georgia, will they actually enhance their lifetime discretionary spending by $500,817? It might turn into $300k, $400k, $600k, or $700k. I don’t assume you possibly can have excessive confidence it’ll be $500k in actual life. All you possibly can say is that promoting and transferring is directionally helpful if the assumptions aren’t too far off.

The Roth conversion video from MaxiFi reveals that the conversion quantity being thought of would increase the annual discretionary spending from $75,739 to $76,109 primarily based on a set of assumptions. I’d name this consequence a toss-up. The $370 distinction is simply too small as a result of it’s lower than 0.5% of the annual discretionary spending. Changing that quantity in actual life may very well be higher or it may very well be worse. I can’t even say it’s directionally helpful. I’d search for strikes that make an even bigger distinction.

Monte Carlo

The Premium model of MaxiFi consists of Residing Normal Monte Carlo®, which simulates how completely different funding methods and spending behaviors affect your residing normal. The $40 worth distinction between the Stand model and the Premium model within the first yr isn’t a lot. You would possibly as nicely get the Premium model to see if the Monte Carlo studies are useful however I discover the usual studies extra helpful than the Monte Carlo studies.

An issue with Monte Carlo is that it all the time reveals a variety of outcomes. My obtainable spending will be $50k a yr if returns are poor or it may be $200k a yr if returns are good. So do I spend $50k or $200k? If I spend $50k a yr and returns aren’t that unhealthy, I’ll have a ton of cash left that I might’ve loved. If I spend $200k a yr and returns are poor, it gained’t be sustainable. This isn’t distinctive to MaxiFi. That’s simply the character of the beast. No software program can take away this uncertainty.

I discover extra worth within the studies within the Normal model of MaxiFi as a result of I solely use the annual spending from the software program as a metric to match completely different situations. I don’t go by the spending output from the software program for my precise spending. If you wish to save just a little bit of cash, perhaps begin with the Normal model and improve to Premium if you determine to make use of MaxiFi long run.

Assist

MaxiFi has a person’s guide on its assist web site and how-to movies and webinars on YouTube. The corporate additionally gives on-line workplace hours twice a month to reply questions. In case you can’t determine find out how to mannequin one thing, you possibly can ship an e-mail to MaxiFi customer support and so they’ll inform you. In order for you a MaxiFi professional to evaluation your plan and provide help to interpret the outcomes, it’s $250 for a one-hour video session. I get the sense that they actually wish to provide help to make good monetary selections with the software program.

Different Software program

I’m glad with MaxiFi general. It’s cheap and helpful to mannequin large monetary selections. No software program can predict the long run or take away uncertainty however you don’t must throw up your fingers and depart large monetary selections to intestine emotions.

It’s unrealistic to count on any software program to provide you a withdrawal plan that gained’t result in having a giant pile of cash on the finish when returns are good or having to regulate the spending down when returns are poor. That’s not how I exploit MaxiFi.

Set a variety of assumptions and consider the big selection of outcomes. You continue to gained’t know the way precisely a giant monetary determination will prove in actual life however you’ll have some thought of a spread and perceive what is going to affect the outcomes. It’s a steal to pay solely $109 or $149 for a software that can assist you make large monetary selections which can be one-time, all-or-nothing, and expensive to modify.

MaxiFi isn’t the one monetary planning software program. I can’t say it’s the most effective as a result of I haven’t used many different software program to match. I solely realize it’s extra highly effective than the free Constancy retirement calculator. NewRetirement and Pralana are in the identical $100 – $150 worth vary. When you’ve got large monetary selections arising and also you’re unsure which software program to make use of, strive all of them and choose your favourite. I’m going to purchase Pralana to strive it when my MaxiFi license expires.

Say No To Administration Charges

In case you are paying an advisor a proportion of your belongings, you’re paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.