When mortgage charges surged off their file lows in early 2022, the housing market floor to a halt.

Within the span of lower than 10 months, 30-year fastened mortgage charges climbed from the low-3% vary to over 7%.

Whereas a 7% mortgage charge is traditionally “cheap,” the share change in such a brief interval was unprecedented.

Mortgage charges elevated about 120% throughout that point, which was really worse than these Nineteen Eighties mortgage charges you’ve heard about when it comes to velocity of change.

The fast ascent of rates of interest was extreme sufficient to introduce us to a brand new phrase, mortgage charge lock-in.

Briefly, current householders turned trapped of their properties seemingly in a single day as a result of they couldn’t go away their low charges behind and change them for a lot increased ones.

Both as a result of it was cost-prohibitive or just unappealing to take action.

And there isn’t a fast repair as a result of your typical house owner has a 30-year fastened mortgage within the 2-4% vary.

Mortgage Charges Have Come Down, However What About Mortgage Quantities?

There’s been a lot deal with mortgage charges that I typically really feel like everybody forgot about sky-high mortgage quantities.

Mortgage charges climbed as excessive as 8% a yr in the past, however have since fallen to round 6%. And could be had for even decrease for those who pay low cost factors.

So in some regard, mortgage charge lock-in has eased, but housing affordability stays constricted.

For the standard residence purchaser who wants a mortgage to get the deal accomplished, there are two most important parts of the acquisition resolution. The asking worth and the rate of interest.

As famous, charges are quite a bit increased than they was once, however have come down about two proportion factors from their 2023 highs.

The 30-year fastened hit 7.79% in the course of the week ended October twenty sixth, 2023, which wasn’t far-off from the twenty first century excessive of 8.64% set in Could 2000, per Freddie Mac.

Nevertheless, residence costs haven’t come down. Whereas many appear to suppose there’s an inverse relationship between mortgage charges and residential costs, it’s merely not true.

Certain, appreciation could have slowed from its unsustainable tempo, however costs continued to rise regardless of markedly increased charges.

And if we think about the place residence costs had been pre-pandemic to the place they stand right now, they’re up about 50% nationally.

In sure metros, they’ve risen much more. For instance, they’re up about 70% in Phoenix since 2019, per the newest Redfin knowledge.

So while you have a look at how mortgage charges have come down, you would possibly begin to focus your consideration on residence costs.

Whereas a 5.75% mortgage charge appears pretty palatable at this juncture, it may not pencil when mixed with a mortgage quantity that has doubled.

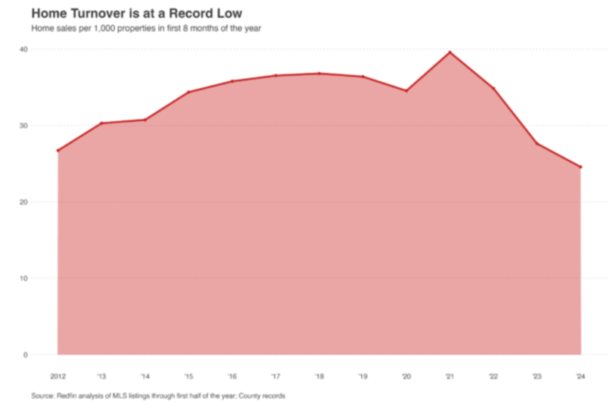

This would possibly clarify why simply 2.5% of properties modified fingers within the first eight months of 2024, per Redfin, the bottom turnover charge in many years. Listings are additionally on the lowest degree in over a decade (since at the very least 2012).

An Instance of Mortgage Quantity Lock-In

| $265k gross sales worth | $450k gross sales worth | |

| Mortgage Quantity | $212,000 | $360,000 |

| Curiosity Fee | 3.5% | 5.75% |

| P&I Fee | $951.97 | $2,100.86 |

| Fee Distinction | n/a | $1,148.89 |

Let’s think about a median-priced residence in Phoenix, Arizona. It was once $265,000 again in August 2019, per Redfin.

Right now, it’s nearer to $450,000. Sure, that’s the 70% enhance I referred to earlier. Now let’s think about the residence purchaser put down 20% to keep away from PMI and get a greater mortgage charge.

We is likely to be a charge of three.50% on a 30-year fastened again in mid-2019. Right now, that charge could possibly be nearer to five.75%.

After we think about each the upper mortgage charge and far increased mortgage quantity, it’s a distinction of roughly $1,150 monthly. Simply in principal and curiosity.

The down fee can also be $90,000 versus $53,000, or $37,000 increased, which could possibly be deal-breaker for a lot of.

This explains why so few persons are shopping for properties right now. The one-two punch of a better mortgage charge AND increased gross sales worth have put it out of attain.

However what’s attention-grabbing is that if the mortgage quantity was the identical, the distinction would solely be about $285, even w/ a charge of 5.75%.

So you possibly can’t actually blame excessive charges an excessive amount of at this level. Certain, $300 is more cash, but it surely’s not that rather more cash for a month-to-month mortgage fee.

And it’s quite a bit higher than the $1,150 distinction with the upper mortgage quantity.

In different phrases, you could possibly argue that current householders trying to transfer aren’t locked in by their mortgage charge a lot as they’re the mortgage quantity.

What You Can Do to Fight Mortgage Quantity Lock-In

In case you already personal a house and are struggling to understand how a transfer could possibly be doable, there’s a doable resolution.

I really had a buddy do that final spring. He was transferring into a much bigger residence in a nicer neighborhood, regardless of holding a 2.75% 30-year fastened mortgage charge.

To cope with the sharp enhance in curiosity, he used gross sales proceeds from the sale of his outdated residence and utilized them towards the brand new mortgage.

The consequence was a a lot smaller stability, regardless of a higher-rate mortgage. This meant far much less curiosity accrued, regardless of month-to-month funds being increased.

He did this when charges had been within the 7% vary. There’s a superb probability he’ll apply for a charge and time period refinance to get a charge within the 5s, at which level he can go together with a brand new 30-year time period and decrease his month-to-month.

If he prefers, he can make additional funds to principal to proceed saving on curiosity, or just benefit from the fee reduction.

Both approach, pulling down the mortgage quantity to one thing extra akin to what he had earlier than, utilizing gross sales proceeds, is one method to bridge the hole.

And the massive silver lining for lots of current locked-in householders is that they received in low cost and have a ton of residence fairness at their disposal.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Observe me on Twitter for decent takes.